As China's cotton yarn imports fell in April 2024, ripple effects felt in global trade

China's cotton yarn imports witnessed a significant decline in April 2024, raising concerns about the global cotton yarn trade and its impact on key players like India.

The fall

China's cotton yarn imports plummeted to 110,900 tons in April 2024, a staggering 35 per cent decrease compared to March (170,000 tons). This level is comparable to April 2023's import volume. The unit price of imported cotton yarn rose to $2.48/kg in April, diminishing the cost-effectiveness of imports compared to the previous period. Rising overseas cotton prices further narrowed the import window.

Domestic demand for imported yarn is price-sensitive. As international yarn prices increased, Chinese traders either completed their stockpiling or maintained minimal inventory for downstream customers. Meanwhile, the import share of carded single yarn below 8s and combed yarn 30-47s is rising, indicating a preference for these specifications. The decline suggests a weakening demand for imported cotton yarn in China, potentially impacting global yarn producers and exporters.

Impact analysis

The decline in Chinese imports will create a ripple effect across the global cotton yarn trade. Yarn exporters, particularly those in South and Southeast Asia, may face reduced demand and potentially lower prices. Indian yarn exports to China decreased in April to 13,900 tons, down from March. The price sensitivity of Chinese cotton yarn importers and rising international yarn prices make Indian yarn less competitive in the short term. This trend, coupled with the overall import decline, suggests a potential challenge for Indian yarn exporters in the near future. However, the long-term impact remains to be seen.

Table: China's cotton yarn imports (April 2024 vs. March 2024)

|

Month |

Cotton yarn imports (tons) |

Change |

|

April 2024 |

110,900 |

-35% |

|

March 2024 |

170,000 |

A decrease in cotton yarn imports suggests that China might rely more on domestically produced cotton yarn, potentially reducing the demand for raw cotton imports. The decrease in cotton yarn imports also indicates a potential reduction in China's raw cotton demand. This could put downward pressure on global raw cotton prices, impacting cotton-growing countries. The substantial decrease in Chinese cotton yarn imports also suggests a potential contraction in global yarn trade volumes. This could lead to increased competition among yarn exporters for remaining markets.

Shifting import preferences

Data reveals, import share of carded single yarn below 8s and combed yarn 30-47s is rising, potentially indicating a shift towards coarser and higher count yarns. And import share of carded single yarn 8-25s and 25-30s has significantly declined, suggesting lower demand for these specifications.

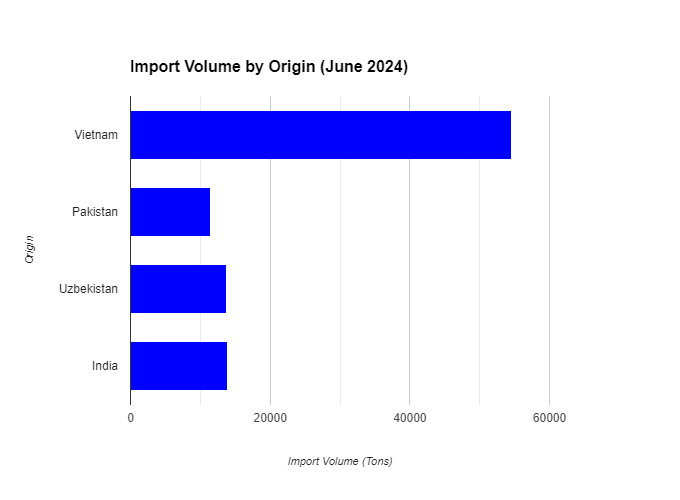

Table: China's Cotton Yarn Imports by Origin (April 2024)

|

Origin |

Import volume (tons) |

Change from March 2024 |

|

Vietnam |

54,600 |

Stable |

|

Pakistan |

11,400 |

-10% |

|

Uzbekistan |

13,700 |

-12% |

|

India |

13,900 |

-10,900 tons |

Vietnamese yarn imports remained relatively stable, while Pakistan, Uzbekistan, and Indian yarns witnessed significant declines. This could be due to price hikes by mills in Pakistani and supply constraints for finer yarns. The decrease in blended cotton yarn imports (13,480 tons) was smaller than the overall cotton yarn import decline. Vietnam remains the dominant supplier (82.5 per cent). This suggests a potential shift in Vietnamese yarn production towards blended yarns due to profitability concerns. Guangdong Province surpassed Zhejiang Province in import share for blended cotton yarn, indicating a potential geographical shift.

The future of China's cotton yarn imports remains uncertain at the moment. Factors like international yarn price trends, domestic cotton yarn production levels, and government policies will influence import volumes.