Bangladesh yarn sourcing in a flux with fight for market share

The Bangladeshi textile industry, a powerhouse in garment exports, is facing a challenge within its supply chain: yarn sourcing. Data from Bangladesh Bank reveals yarn imports are on the rise while imports of other textile raw materials are declining.

Shifting Share: Domestic vs. Imports

Bangladesh Bank statistics reveals yarn import growth of over 10 per cent for July-March FY 2023-24 compared to the same period in FY 2022-23. This translates to a rise from $2.10 billion to $2.32 billion.

However, there has been a decline in other raw material imports. Raw imports fell cotton 24.9 per cent; textile & articles fell 8.2% ; staple fibre was down 6.1 per cent; dying and tanning materials dipped 3.1 per cent compared to July-March FY 2022-23.

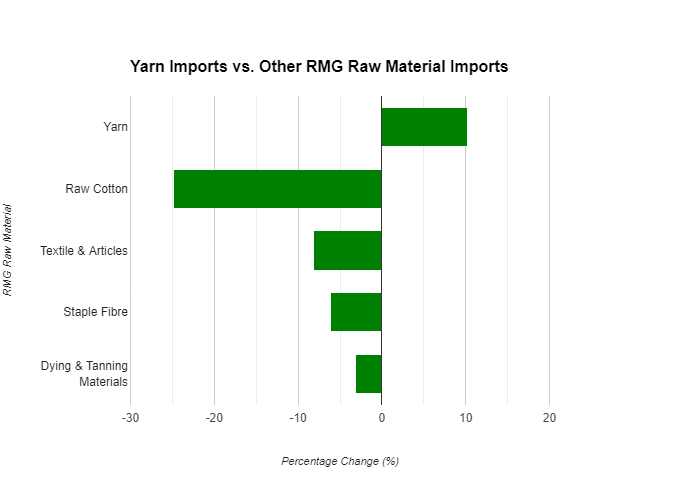

Table: Yarn imports vs. other RMG raw material imports

|

Yarn |

+10.2% |

|

Raw Cotton |

-24.90% |

|

Textile & Articles |

-8.20% |

|

Staple Fibre |

-6.10% |

|

Dying & Tanning Materials |

-3.10% |

Source: Bangladesh Bank

Several factors contribute to this trend

- Price disparity: RMG exporters find imported yarn, particularly from India, China, and Pakistan, to be cheaper than domestically produced yarn.

- Production cost challenges: Local spinners struggle with high utility costs (electricity, gas) and limited gas supply, hindering full capacity utilization and pushing up yarn prices.

- Policy support asymmetry: BTMA alleges "dumping prices" by foreign competitors who benefit from government subsidies in their home countries.

This shift towards imported yarn has negative consequences. Local yarn consumption keeps the US dollar circulating within Bangladesh. Domestic spinners are losing business to foreign competitors, hindering the growth of the local spinning sector. Increased imports lead to capital outflow. And if the trend continues, many textile mills may face closure due to a lack of competitiveness. Moreover, for a robust garment industry, a strong domestic yarn supply chain is crucial.

Interestingly, the story is not uniform across yarn types. Industry experts say, local mills meet 80 per cent demand for knitwear yarn (used in T-shirts, polos, etc.) And 35-40 per cent demand for woven yarn (used in dress shirts, trousers, etc.) with a higher dependence on imports. This suggests a stronger domestic presence in knitwear yarn production, possibly due to simpler technology or lower raw material dependence.

Even as Bangladesh's garment exports continue to thrive, reaching $37.20 billion during July-March 2023-24, increasing reliance on imported yarn creates a tension. Indeed, there are short-term benefits as cheaper imported yarn allows exporters to maintain price competitiveness in the global market. However, in the long-term risk a weak domestic yarn industry undermines the ‘backyard linkage supply’ crucial for long-term export sustainability, argues BGMEA.

Navigating challenges

To tide over the problem, Bangladeshi textile industry needs a multi-pronged approach.

- Cost reduction: Domestic producers need to find ways to reduce production costs through improved efficiency and exploring alternative energy sources.

- Government support: Policy interventions to level the playing field with competitors, like subsidies or tax breaks, could be explored.

- Technological upgradation: Investing in modern technologies could enhance efficiency and product quality.

- Focus on specialization: Local mills may benefit from specializing in niche yarn types or catering to specific garment segments.