China's spandex slump, prices fall amidst capacity expansion

China's spandex sector passed through challenging times in the first quarter of 2025. While the broader Chinese economy received government stimulus and showed resilience on the supply side, the spandex market grappled with falling prices, concerns stemming from rapid capacity expansion in related industries, and softer downstream demand. A look at the market indicators and broader economic context during the period highlights this scenario.

Broader economic context

The spandex sector’s performance occurred against a backdrop of mixed signals from the overall Chinese economy at the start of 2025. While industrial production and investment showed strength, consumer demand remained tentative, and export momentum faced hurdles.

Table: China’s economic indicators in early 2025

|

Indicator |

Period |

Value / Status |

|

Caixin Manufacturing PMI |

Jan 2025 |

50.1 (Slight Expansion) |

|

Fixed Asset Investment |

Jan-Feb 2025 |

+4.1% YoY |

|

Retail Sales Growth |

Jan-Feb 2025 |

+4.0% YoY |

|

Export Growth |

Jan-Feb 2025 |

+2.3% YoY (Slowdown) |

The table above reveals the mixed economic environment influencing the spandex market. While manufacturing activity continued (PMI > 50) and investment grew, consumer-facing retail sales growth was modest, and the significant slowdown in export growth pointed to falling external demand. This backdrop contributed to cautious downstream purchasing.

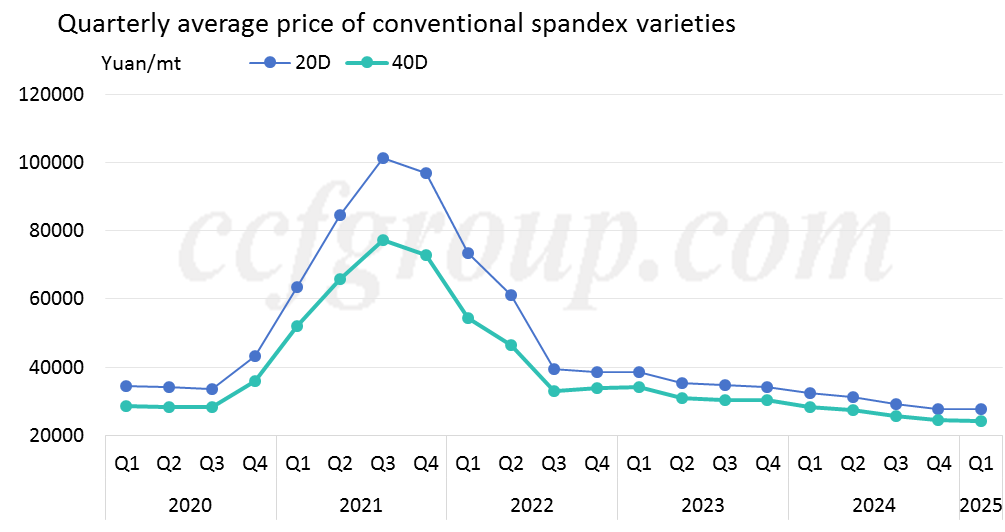

Price volatility and downside of expanding capacity

After a period of relative stability observed mid-quarter, the spandex market saw a return to weakness as Q1 concluded. Price levels seen in late February provided a temporary floor before softening again.

Table: China spandex price snapshot (late Feb 2025)

|

Region / Type |

Denier |

Mainstream Price (RMB/ton) |

|

Zhejiang |

20D |

29,500 |

|

Zhejiang |

40D |

25,000 |

|

Jiangsu (Ref.) |

40D |

26,000 |

|

Fujian |

20D |

31,500 |

|

Fujian |

30D |

28,500 |

|

Fujian |

40D |

25,500 |

The prices in late February as shown in the above table indicate the levels producers were achieving mid-quarter, showing some regional variations. However, reports by early April indicated a weakening trend from these levels, suggesting demand was insufficient to maintain price stability despite relatively firm raw material costs earlier in the quarter. The latest tariffs war also added to downward pressure.

While specific Q1 2025 spandex capacity startups are not available in recent reports, the sector operates within a broader context of significant build-out across China's petrochemical industries. This upstream expansion increases overall material supply, potentially intensifying competition across related segments this led to margin pressures for intermediate products like spandex. The market softness and competitive pressures were reflected in operational indicators during the quarter.

Table: China spandex market indicators (Q1 2025)

|

Indicator |

Period |

Value / Status |

|

Operating Rate |

Early Jan 25 |

Declined below 80% |

|

Price Trend |

Late Q1 25 |

Weakening |

|

Inventory Action |

Early Apr 25 |

Plants Active Sellers |

As the table shows, the quarter began with lower operating rates, indicating producers were already adjusting output. The subsequent price decline towards the end of the quarter, coupled with plants actively trying to sell inventory, suggests that underlying demand failed to meet supply expectations, leading to increased pressure on producers.

Thus domestic consumer confidence remained relatively weak in China, translating to cautious purchasing from downstream textile and apparel manufacturers. Slow recovery in weaving activity post-holidays and concerns over export markets further dampened sentiment.

Thus while the long-term structural demand for spandex remains positive, due to global trends in sportswear and comfort apparel, the near-term outlook for China's spandex sector appears cautious. The data from Q1 2025 points towards a market grappling with weak pricing, adjusting operating rates, and facing competitive pressures amplified by broader industry capacity growth and uncertain end-use demand. Navigating these challenges will be key for the sector through the remainder of 2025.

China's spandex slump, prices fall amidst capacity expansion

Meta Description: Why did China's spandex sector struggle in Q1 2025? How did economic indicators affect prices? Find out the market challenges.

China's spandex sector passed through challenging times in the first quarter of 2025. While the broader Chinese economy received government stimulus and showed resilience on the supply side, the spandex market grappled with falling prices, concerns stemming from rapid capacity expansion in related industries, and softer downstream demand. A look at the market indicators and broader economic context during the period highlights this scenario.

Broader economic context

The spandex sector’s performance occurred against a backdrop of mixed signals from the overall Chinese economy at the start of 2025. While industrial production and investment showed strength, consumer demand remained tentative, and export momentum faced hurdles.

Table: China’s economic indicators in early 2025

|

Indicator |

Period |

Value / Status |

|

Caixin Manufacturing PMI |

Jan 2025 |

50.1 (Slight Expansion) |

|

Fixed Asset Investment |

Jan-Feb 2025 |

+4.1% YoY |

|

Retail Sales Growth |

Jan-Feb 2025 |

+4.0% YoY |

|

Export Growth |

Jan-Feb 2025 |

+2.3% YoY (Slowdown) |

The table above reveals the mixed economic environment influencing the spandex market. While manufacturing activity continued (PMI > 50) and investment grew, consumer-facing retail sales growth was modest, and the significant slowdown in export growth pointed to falling external demand. This backdrop contributed to cautious downstream purchasing.

Price volatility and downside of expanding capacity

After a period of relative stability observed mid-quarter, the spandex market saw a return to weakness as Q1 concluded. Price levels seen in late February provided a temporary floor before softening again.

Table: China spandex price snapshot (late Feb 2025)

|

Region / Type |

Denier |

Mainstream Price (RMB/ton) |

|

Zhejiang |

20D |

29,500 |

|

Zhejiang |

40D |

25,000 |

|

Jiangsu (Ref.) |

40D |

26,000 |

|

Fujian |

20D |

31,500 |

|

Fujian |

30D |

28,500 |

|

Fujian |

40D |

25,500 |

The prices in late February as shown in the above table indicate the levels producers were achieving mid-quarter, showing some regional variations. However, reports by early April indicated a weakening trend from these levels, suggesting demand was insufficient to maintain price stability despite relatively firm raw material costs earlier in the quarter. The latest tariffs war also added to downward pressure.

While specific Q1 2025 spandex capacity startups are not available in recent reports, the sector operates within a broader context of significant build-out across China's petrochemical industries. This upstream expansion increases overall material supply, potentially intensifying competition across related segments this led to margin pressures for intermediate products like spandex. The market softness and competitive pressures were reflected in operational indicators during the quarter.

Table: China spandex market indicators (Q1 2025)

|

Indicator |

Period |

Value / Status |

|

Operating Rate |

Early Jan 25 |

Declined below 80% |

|

Price Trend |

Late Q1 25 |

Weakening |

|

Inventory Action |

Early Apr 25 |

Plants Active Sellers |

As the table shows, the quarter began with lower operating rates, indicating producers were already adjusting output. The subsequent price decline towards the end of the quarter, coupled with plants actively trying to sell inventory, suggests that underlying demand failed to meet supply expectations, leading to increased pressure on producers.

Thus domestic consumer confidence remained relatively weak in China, translating to cautious purchasing from downstream textile and apparel manufacturers. Slow recovery in weaving activity post-holidays and concerns over export markets further dampened sentiment.

Thus while the long-term structural demand for spandex remains positive, due to global trends in sportswear and comfort apparel, the near-term outlook for China's spandex sector appears cautious. The data from Q1 2025 points towards a market grappling with weak pricing, adjusting operating rates, and facing competitive pressures amplified by broader industry capacity growth and uncertain end-use demand. Navigating these challenges will be key for the sector through the remainder of 2025.