Chinese polyester exports rise in July amidst market divergence.

The Chinese polyester industry witnessed a surge in exports in July, reaching 1.047 million tons, marking a 197,000-ton increase year-on-year. However, this figure also represents a 67,000-ton decrease compared to June. The overall export performance for polyester products in 2024 has been favorable, with total exports from January to July reaching 7.185 million tons, an 802,000-ton increase year-on-year. Despite this positive trend, the market continues to exhibit disparities across different product categories.

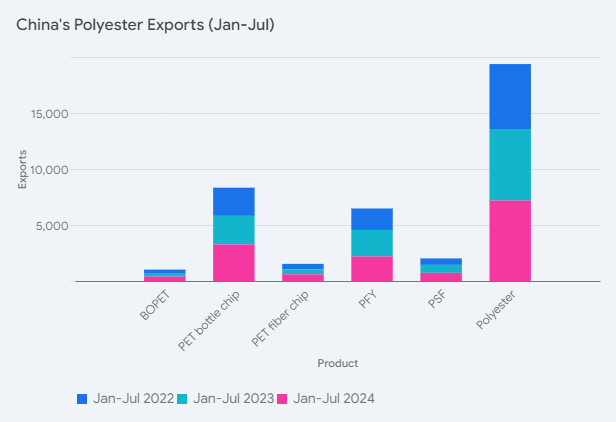

Export performance

The export growth in July was primarily driven by products such as PET bottle chips, which saw a significant year-on-year increase of 182,000 tons. Other products, including BOPET and PET fiber chips, also contributed to the overall export growth. However, filament yarn exports saw a decline of 21,000 tons year-on-year. The cumulative export data from January to July further highlights the market discrepancy. While bottle-grade PET exports led growth with a 712,000-ton increase, filament yarn exports faced a decline of 177,000 tons compared to the same period in 2023.

Domestic consumption vs exports

The decline in filament yarn and staple fiber exports in June and July 2024 raises questions about the dynamics between domestic consumption and exports. Two potential explanations emerge.

Table: China’s polyester exports

|

Product |

Jan-Jul 2022 |

Jan-Jul 2023 |

Jan-Jul 2024 |

Jan-Jul 2023 Y-o-Y |

Jan-Jul 2024 Y-o-Y |

|

PFY |

1918 |

2367 |

2190 |

449 |

-177 |

|

PSF |

577 |

708 |

731 |

131 |

23 |

|

PET fiber chip |

491 |

439 |

598 |

-52 |

159 |

|

PET bottle chip |

2516 |

2552 |

3265 |

36 |

712 |

|

BOPET |

300 |

316 |

400 |

17 |

84 |

|

Polyester |

5801 |

6383 |

7185 |

582 |

802 |

One reason could be that domestic filament yarn and staple fiber producers might be adjusting their strategies to prioritize price support in the domestic market, making export negotiations less attractive. Weak overseas demand could be another reason. A decline in overseas demand could lead to reduced procurement of raw materials, impacting export volumes.

Moreover the contrasting performance of different product categories underscores the market differentiation within the polyester industry. While the non-fiber segment, including PET chips and films, thrived in June and July, filament yarn and staple fiber exports faced challenges. This difference suggests varying market dynamics and demand patterns across different product segments.

Thus Chinese polyester industry's export performance in July 2024 reflects a complex market landscape characterized by growth, divergence, and strategic shifts. While overall export remains positive, the disparities across product categories and the evolving dynamics between domestic consumption and exports warrant close attention. As the industry navigates these challenges, understanding market trends and adapting strategies will be crucial for sustained growth and success in the global marketplace.