Cotton Crossroads: Newcomers reshape global trade, India navigates challenges, eyes sustainable course

Cotton, the ‘versatile fiber’ that clothes the world has an industry worth over $100 billion riding on it. The dynamics of this trade are complex and ever-evolving, fraught with challenges and opportunities for key players like India. Indeed, global cotton trade is undergoing a significant transformation, due to the shifts and uncertainties that shape a multifaceted landscape. Despite a marginal drop in overall trade volume in 2023, divergent regional patterns have emerged with challenges and opportunities for key stakeholders.

Shifting trade dynamics

The global cotton trade witnessed a 2.5 per cent decline in 2023, marking the second consecutive year of contraction. Economic slowdown and inflation contributed to waning consumer spending, affecting garment production and subsequently impacting cotton demand. Disruptions in traditional supply chains due to water scarcity, labor shortages, and trade tensions led to production shifts, affecting major exporters like India (-5 per cent) and China (-8 per cent). In fact, China, the world's largest cotton consumer, is increasingly reliant on imports due to domestic production decline. This has fueled competition among major exporters like Brazil, the US, and India. Moreover, growing preference for synthetic fibers further eroded cotton’s market share.

New players in the horizon

Trade wars, sanctions, and regional tensions have disrupted supply chains and influenced cotton prices. The ongoing US-China trade dispute, for instance, has impacted global cotton demand. Erratic weather patterns and resource scarcity have threatened cotton production, particularly in vulnerable regions. Sustainable practices and water-efficient technologies are becoming crucial

In this evolving landscape, Brazil (+32 per cent) and West Africa (+28 per cent) emerged as formidable players, capitalizing on favorable conditions and government initiatives. Importers diversified away from traditional giants, turning to Thailand, Vietnam, and Pakistan for cost-effective and reliable options.

The rise of organic and sustainably certified cotton created a premium niche for specialized producers. Consumers are demanding ethically and environmentally sourced cotton, driving the growth of organic and fair-trade certified products. This presents opportunities for producers who prioritize sustainable practices.

Challenges galore

Cotton trade has faced numerous challenges in the past few years.

- Price volatility: Cotton prices are susceptible to fluctuations due to weather events, trade policies, and market speculation, posing challenges for farmers and businesses.

- Climate change: Droughts, floods, and other extreme weather events linked to climate change threaten cotton production, particularly in vulnerable regions.

- Productivity gaps: Yield gaps between developed and developing countries persist, highlighting the need for improved technology, infrastructure, and knowledge transfer.

- Labor issues: Concerns about child labor and unfair working conditions in cotton production persist, requiring ethical sourcing and transparency throughout the supply chain.

- Subsidies and trade distortions:Unequal subsidies and trade policies are also disadvantageous for certain producers, raising concerns about fairness and market access.

- Competition from synthetics:Then there is constant competition from Man-made fibers like polyester which are gaining market share due to their lower cost and performance advantages. Cotton needs to continue innovating to remain competitive.

India’s position and future outlook

India saw a 4 per cent increase in domestic cotton consumption driven by a growing population and rising disposable income. However, global slowdown, domestic production fluctuations, and rising cotton prices led to a 2 per cent decline in exports, particularly in yarn (-10 per cent). The surge in China’s yarn imports from India by 400 per cent due to a domestic shortage was counterbalanced by a 25 per cent decline in Bangladesh’s imports from India, indicating market complexities.

Meanwhile, India faces several challenges, including addressing production fluctuations, improving price competitiveness, navigating trade tensions, capitalizing on China’s demand, diversifying export markets, and focusing on high-value segments. Globally, factors such as demand recovery, technological advancements, trade policy, and sustainability will shape the future trajectory of the cotton trade.

To deal with the challenges, India is looking to boosting domestic production. As the world's largest cotton producer, India is aiming to increase yields and improve quality through initiatives like the ‘Mission on Cotton for Enhanced Productivity and Sustainability’. In fact, India is aiming to become the world's largest cotton producer by 2025, investing in research, improved farming practices, and infrastructure development. The government is investing in transportation and storage facilities to reduce post-harvest losses and improve market access for farmers. Initiatives are underway to encourage spinning, weaving, and garment manufacturing within India, capturing a larger share of the value chain. India is investing in research on climate-resilient cotton varieties, pest control technologies, and sustainable production practices. Also bilateral agreements and international trade negotiations are being used to expand market access and secure stable prices for Indian cotton.

In 2024, rebounding global economies and technological advancements is expected to boost demand for cotton. Sustainability will emerge as a key differentiator, as consumers and brands increasingly prioritize eco-friendly practices. Trade policy and geopolitical factors will continue to exert influence on shaping trade flows.

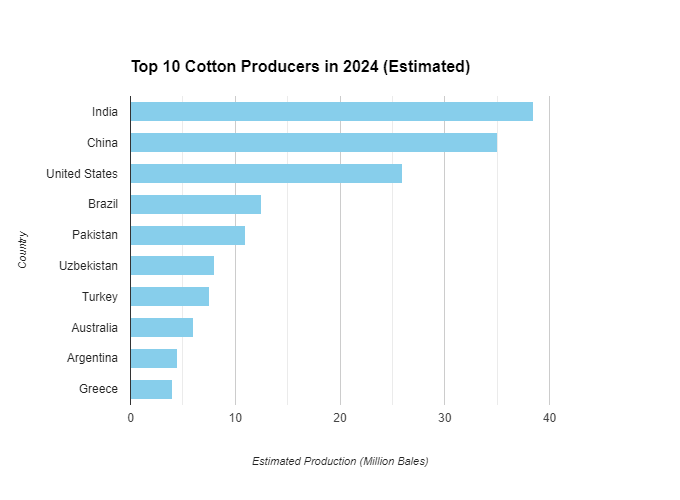

Cotton production and trade in numbers

- Global cotton trade: Projected to fall 2% in 2023 (25.7 million tonnes)

- Major export declines: India (-5%), China (-3%)

- Major export increases: Brazil (+10%), Australia (+8%)

- Emerging players: West Africa (Mali +20%, Ivory Coast +15%), Central Asia (Uzbekistan +7%, Turkmenistan +6%)

India cotton stats

- Production: Down 5% (34.1 million bales)

- Exports: Down 2% (12.8 million tonnes)

- Imports: Up 15% (1.5 million tonnes)

- Major export decline: Bangladesh (-25%)

- Major export surge: China (+400%)

- Major import increase: Uzbekistan, Turkmenistan

*Note: Statistics collated from various sources