India's nylon industry sees a tug-of-war between producers and weavers

India’s nylon sector is facing internal conflict as the spinning and weaving industries present opposite demands to the government. The Nylon Spinners Association (NSA) seeks the mandatory enforcement of the Quality Control Order (QCO), an anti-dumping duty, or a 10 per cent customs duty to curb rising imports. They argue that an influx of cheap Chinese imports has severely impacted domestic producers, citing a surge in Chinese market share from 1 per cent to 85 per cent in six years.

While spinners are demanding higher protection to combat the influx of cheap Chinese imports, weavers argue that domestic production falls short in terms of both quantity and quality. The government is now tasked with the challenging task of navigating these opposing viewpoints and formulating policies that promote the overall growth and sustainability of the industry.

Nylon market overview

India’s nylon market was valued at almost $2.5 billion in 2023. The market is expected to grow at a CAGR of around 8 per cent between 2023 and 2028. This rate of growth could push up the market to touch $3.8 billion by 2028. While domestic consumption is robust, India heavily relies on imports, particularly from China. This dependence has escalated tensions within the industry.

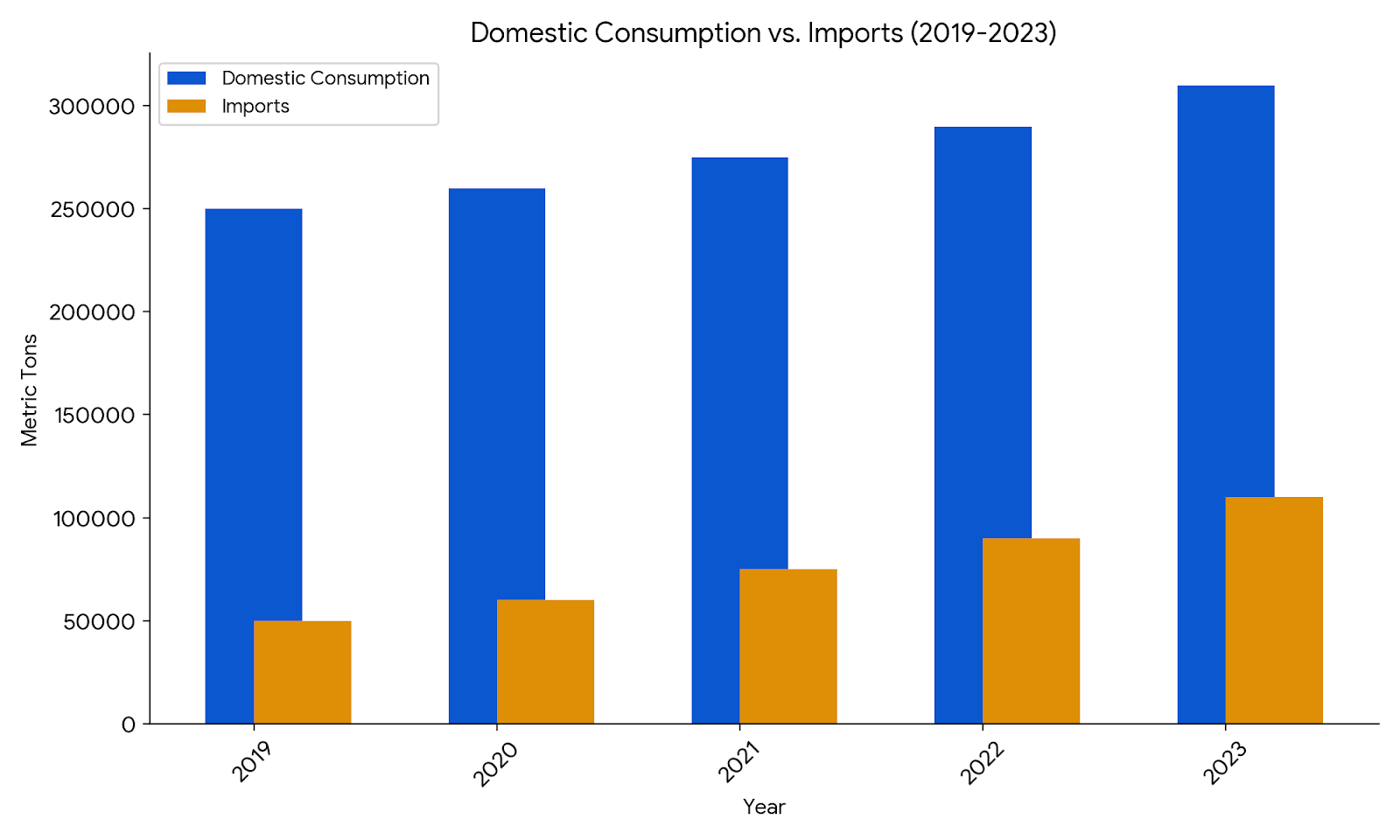

Table: Domestic consumption and imports

|

Year |

Domestic consumption (metric tons) |

Imports (metric tons) |

|

2019 |

250,000 |

50,000 |

|

2020 |

260,000 |

60,000 |

|

2021 |

275,000 |

75,000 |

|

2022 |

290,000 |

90,000 |

|

2023 |

310,000 |

110,000 |

Imports, particularly from China, have witnessed substantial increase in recent years. This increase has been a major point of contention within the industry. The removal of anti-dumping duty on nylon filament yarn led to a dramatic rise in Chinese imports, capturing over 85 per cent of the market.

The nylon market is segmented based on product type (nylon 6, nylon 66, others), application (textile, automotive, engineering plastics, others), and end-use industry (apparel, automotive, electrical & electronics, others).

Stakeholders concerns

The Nylon Spinners Association (NSA) argues there interest is in conflict. "The domestic nylon industry is suffering significant losses due to the influx of cheaper Chinese supplies." They have urged the government to implement corrective measures such as the QCO, anti-dumping duty, or higher customs duty to protect the industry. However, the weaving and knitting industry has a contrary view. "Indian producers do not produce several varieties of nylon yarn, and the quality of domestically produced yarn is inferior." They say, NSA's demands will restrict competition and limit access to raw materials.

In fact, the current situation in the nylon industry echoes the past experiences of the polyester and viscose sectors. The implementation of the QCO in these sectors led to increased domestic production but also resulted in higher prices and limited competition. This raises concerns that similar measures in the nylon industry could have unintended consequences.

The government now faces a delicate task of balancing the interests of nylon spinners and weavers. While protecting the domestic industry is crucial, ensuring access to quality raw materials at competitive prices is equally important for the downstream sectors. It could come up with several solutions.

It could go forward with phased implementation of QCO. To ensure a smooth transition, the QCO could be implemented in phases, allowing domestic producers to ramp up production and improve quality. The important this is to encouraging research and development that can help domestic producers develop new varieties of nylon yarn and improve the quality of existing products. And providing training and skill development programs to workers in the nylon industry can enhance productivity and efficiency.