India's Woven Cotton Fabrics Market: A balancing act between tradition and transformation

India, a nation deeply rooted in textile heritage, continues to play a pivotal role in the global woven cotton fabrics market. While demand for versatile textiles remains strong worldwide, market growth is expected to decelerate in the coming decade. Recent projections suggest a stagnant Compound Annual Growth Rate (CAGR) of +0.0 per cent in volume and a modest +1.0 per cent increase in value from 2024 to 2035. Despite this slow pace, India’s domestic market presents a complex scenario of both opportunities and challenges.

Global consumption of woven cotton fabrics

In 2024, global consumption of woven cotton fabrics reached 15 billion sq. mt, marking a 3.3 per cent increase from the previous year. However, the overall growth trajectory has been slower, with an average annual increase of +1.3 per cent from 2013 to 2024. The market value stood at $108.8 billion, a slight 2.4 per cent rise. China remains the dominant consumer, accounting for 4.5 billion sq. mt (30 per cent of the global volume) valued at $25.4 billion, followed by the US, which consumes 1.8 billion sq. mt valued at $11.2 billion. India ranks third, consuming 894 million sq. mt. China continues to lead in production as well, contributing 12 billion sq. mt (58 per cent of global output), while the US produces 1.4 billion sq. mt and Pakistan contributes 1.1 billion sq. mt.

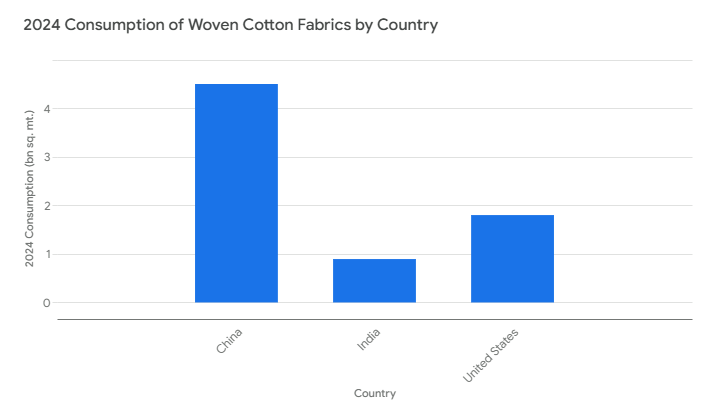

Table: Woven cotton fabrics consumption growth (volume)

|

Country |

2024 Consumption (bn sq. mt.) |

CAGR (2013-2024) |

|

China |

4.5 |

+2.0 per cent |

|

United States |

1.8 |

+1.2 per cent |

|

India |

0.894 |

+3.1 per cent |

The international trade of woven cotton fabrics is a complex web of imports and exports. In 2024, imports declined by 1.1 per cent to 4.5 billion sq. mt, valued at $18 billion. Similarly, exports fell by 1.4 per cent to 9.3 billion sq. mt, with a market value of $19.5 billion. The US, Bangladesh, and Italy remain major importers, with the most widely traded category being cotton woven fabric containing 85 per cent or more by weight of cotton and weighing not more than 200 g/m². This segment dominates both import and export markets, emphasizing its versatility in textile manufacturing.

India scenario

India remains a major producer of woven cotton fabrics, ranking third globally. However, its production growth has been modest, with a CAGR of just +0.5 per cent from 2013 to 2024. This slow expansion is attributed to fluctuating cotton prices, infrastructure bottlenecks, and competition from more efficient producers like China. Despite its strong production base, India’s share in global exports has seen a decline. In 2024, it exported 146 million sq. mt of woven cotton fabrics, valued at $1.7 billion, representing 8.7 per cent of global exports. Meanwhile, its import volume reached 230 million sq. mt. The annual growth rate of export value from 2013 to 2024 has been negative (-0.7 per cent), indicating market erosion.

India’s average export price for woven cotton fabrics was $12 per square meter in 2024, significantly above the global average. This reflects India’s focus on higher-value products and specialized textiles. However, the average annual price growth from 2013 to 2024 was negative (-1.6 per cent), signaling pricing pressure. The industry faces several challenges, including competition from Bangladesh and Vietnam, fluctuating cotton prices, and infrastructure constraints. Lower production costs in competing nations make them more attractive in the global market, while inadequate logistics and outdated production facilities hinder efficiency in India.

Advantage India

Despite these challenges, India has significant advantages. Its abundant cotton resources, rich textile craftsmanship, growing domestic demand, and government support for exports and modernization offer substantial growth potential. To remain competitive, India must invest in technology and modernization by upgrading production facilities and adopting sustainable practices. Enhancing productivity and efficiency by streamlining operations and improving resource utilization will also be key. Diversifying the product mix to focus on high-value and specialized textiles can help capture premium market segments, while strengthening export competitiveness by improving quality and reducing costs will be essential. Promoting sustainable cotton farming and ensuring environmental responsibility in textile production will further bolster the industry’s long-term prospects.

India’s woven cotton fabrics market stands at a crossroads. While global growth is expected to slow, India has the potential to maintain its strong position with strategic investments in modernization and efficiency. By addressing challenges and leveraging its strengths, India can continue to be a key player in the evolving global textile market.